Did we just dodge a recession?

Toward the end of 2022, there was an unusually strong consensus that the U.S. economy was headed for a recession in 2023. Yet, so far this year, American consumers have remained resilient, the labor market has remained tight and the housing market has been reinvigorated by an uptick in construction and sale of newly built homes. Even the stock market appears to have regained some swagger as analysts raise their year-end targets for major indices.

Why did 10 consecutive interest rate hikes by the Federal Reserve, which cumulatively pushed interest rates up by 500-basis points, fail to generate a noticeable slowdown in U.S. economic activity?

While issues associated with monetary policy lags and the monetary transmission mechanism have been previously discussed, there are three crucial developments that have not received sufficient attention among economists and market participants that may offer additional insights regarding the somewhat surprising resilience of the U.S. economy so far.

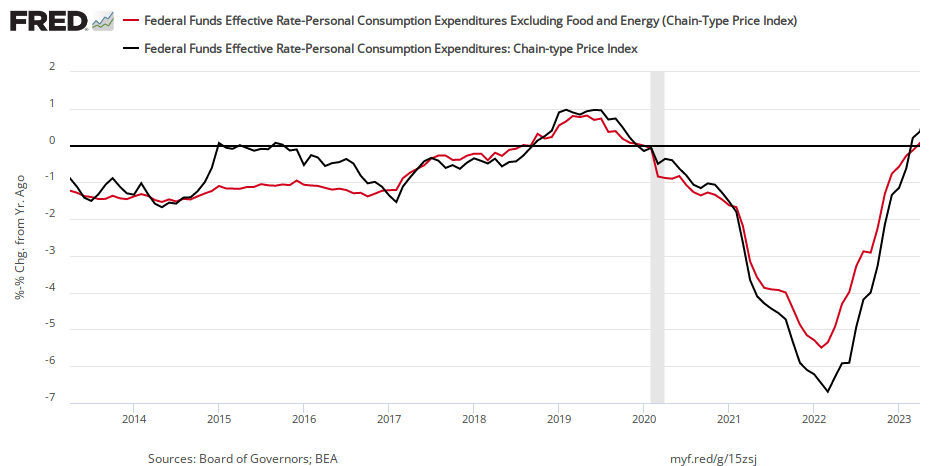

First, it is worth noting that, according to economic theory, it is the real interest rate that matters when it comes to influencing aggregate demand and real economic activity. And it is only when the nominal interest rate exceeds the inflation rate that we attain a positive real interest rate. The so-called “Taylor Principle,” which is widely accepted in central banking circles, recommends that monetary policymakers facing an inflation threat should raise nominal rate by more than one-for-one in response to a persistent increase in inflation.

Interestingly, even though the Fed started raising rates in March 2022, it took a full year for the real policy rate to move into positive territory. This suggests that monetary policy may have reached restrictive territory only recently, and that its impact on real economic activity will become more apparent during the coming months.

The extent to which monetary policy is accommodative or restrictive may also be determined by examining whether or not the real interest rate is above or below the so-called neutral rate — the equilibrium real interest rate that is consistent with maintaining full employment alongside price stability. Based on recent estimates of the real neutral rate for the U.S., it appears that monetary policy during the last year remained accommodative despite multiple rate hikes. Attaining a sufficiently restrictive stance may require further nominal rate hikes or a faster decline in the inflation rate.

Second, global liquidity levels have not been quite as constricted as the flurry of interest rate hikes by major central banks would imply. For example, the Fed’s intervention to prop up troubled regional banks in the U.S. has actually added liquidity into the financial system, offsetting some of the effects associated with its ongoing quantitative tightening program. Significantly, at the global level, the Bank of Japan’s highly accommodative stance continues to contribute positively to global liquidity.

It is noteworthy that global liquidity levels remain elevated and are supporting selective asset markets, such as tech stocks in the U.S. The frenzy surrounding artificial intelligence, the emergence of zero-day options and the ongoing global liquidity provision by key central banks have generated a stunning rally in widely held mega-cap tech stocks. Equity market strength has helped re-inflate household balance sheets and reduced the potency of the asset-price channel of monetary policy transmission.

A third development of note relates to the ongoing resilience of the U.S. consumer. Extraordinary levels of fiscal stimulus in 2020-2021 gave rise to substantial excess savings. As a recent Fed study noted, “households rapidly accumulated unprecedented levels of excess savings — defined as the difference between actual savings and the pre-recession trend — relative to previous recessions. Moreover, despite a rapid drawdown of savings in recent months, there is still a large stock of aggregate excess savings in the economy — some $500 billion….We expect that these excess savings could continue to support consumer spending at least into the fourth quarter of 2023.”

Does all this mean that the U.S. economy will avoid a recession? Although the resilience of the economy in the first half of 2023 has surprised many, it is worth noting that there are dark clouds on the horizon that are still likely to tip the economy into a recession in the coming quarters.

It is now gradually dawning on financial markets that the Fed will have to maintain rates “higher for longer” and that further rate hikes may be on the cards this summer. Risks to the regional banking system remain, and turmoil in the corporate real estate sector poses an ongoing threat to financial stability.

There are also emerging signs that the U.S. labor market may finally be softening as tighter credit conditions for small businesses and declining corporate margins start to affect hiring decisions. Furthermore, the U.S. manufacturing sector may already be in a recession.

So although the resiliency of the economy has certainly surprised many prognosticators, it may be premature to dismiss fears of a recession. Downside risks are likely to become more apparent with monetary policy finally entering the restrictive range. Labor market softness and a potential pullback in consumer spending are also likely to put the brakes on economic activity.

Vivekanand Jayakumar is an associate professor of economics at the University of Tampa.

{kind=link}